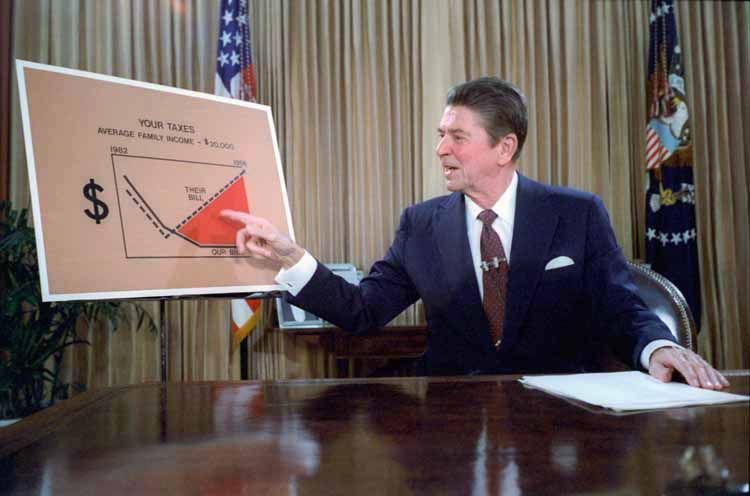

Ronald Reagan gives a televised address from the Oval Office, outlining his plan for Tax Reduction Legislation in July 1981. (Library of Congress via Wikimedia Commons)

Lately, a number of economists associated with the Democratic Party have been engaging in a spirited back-and-forth about the economic impact of Senator Bernie Sanders’ economic program. Those we will call establishment economists are mostly former members of the Council of Economic Advisers (CEA) under Democratic presidents, while those we will call the insurgents tend to be less well known but are, nevertheless, well-credentialed economists. In many respects, the establishment economists are on the right side of the Democratic Party’s political spectrum, while the insurgents are on the left.

The essence of the debate is whether Sanders’ economic plan, which involves a substantial increase in government spending for infrastructure and other programs, is capable of significantly raising the rate of economic growth in the near-term. The establishment economists say that is unlikely if not impossible because it implies an implausibly large increase in the labor force and productivity. The insurgents argue that there is still a great deal of unused capacity in the economy that could come on line quickly if the right policies were followed.

One of us (Galbraith) has already taken sides in that debate, but our purpose today is not to discuss the pros and cons of the Sanders plan. Rather, what struck both of us is the similarity to a debate that took place exactly 35 years ago about the economic impact of Ronald Reagan’s economic plan. One of us (Bartlett) was intimately involved in that debate while the other was a close observer. We viewed the debate from a perch on Capitol Hill where we both worked for the Joint Economic Committee, the congressional counterpart to the CEA.

The establishment in those days, like today, were mostly affiliated with the CEA under Republican presidents. Many identified themselves as “monetarists” associated with Milton Friedman at the University of Chicago who thought that the money supply was the central driver of the macroeconomy. Prominent monetarists in the administration included Jerry Jordan, a member of the 3-person CEA, and Beryl Sprinkel, Under Secretary of the Treasury for Monetary Affairs.

The insurgents were the supply-siders, who had sold Reagan on the idea of a big tax rate reduction modeled on legislation proposed by Rep. Jack Kemp and Senator Bill Roth in 1977. Inside the Reagan administration, they were represented by Larry Kudlow, chief economist for the Office of Management and Budget; Norman Ture, Under Secretary of the Treasury for Tax and Economic Affairs; and Paul Craig Roberts, Assistant Secretary of the Treasury for Economic Policy.

Like now, much of the debate between the two sides involved how much economic growth was capable of rising under Reagan’s proposed policies, and the administration’s economic forecast was the turf upon which the battle was fought. The supply-siders were very optimistic about faster growth and that inflation would fall rapidly. The monetarists thought large growth effects were implausible, given that the Federal Reserve had raised interest rates sharply and was tightening the money supply to squeeze inflation out of the economy. They also thought the fight against inflation would be long and painful.

Standing on the sidelines were mainstream economists, most of whom could probably be called Keynesian. In some ways they agreed with the monetarists, in other ways with the supply-siders. They were not especially enamored with a tax cut, but agreed that it would provide some fiscal stimulus to output and also raise inflation. They thought that Reagan’s proposed increase in defense spending was economically important, something mostly ignored by both the monetarists and the supply-siders. The Keynesians also thought faster growth was implausible as long as Fed policy remained tight.

Arbitrating the monetarist/supply-sider debate were Murray Weidenbaum, chairman of the CEA, who leaned toward the monetarists; David Stockman, director of the Office of Management and Budget, who had been a supply-sider but came to believe that reducing the deficit was paramount; and Treasury Secretary Don Regan, whose main interest was in pleasing the president and tended to side with the supply-siders. Treasury, OMB and the CEA made up the so-called “troika” that established the forecast used for budgetary purposes and Weidenbaum basically had the last word.

The forecast of inflation was the key battleground because it was the most politically important economic statistic, given that the consumer price index rose 13.3 percent in 1979 and 12.5 percent in 1980. The Carter administration’s last forecast, which probably reflected the conventional wisdom among economists, predicted double-digit inflation in 1981 and 1982, tapering down slowly to 6.3 percent by 1986.

According to reporting by John Berry in the Washington Post on February 7, 1981, the preliminary Reagan forecast saw inflation falling in half to 6.5 percent in 1982, 4.5 percent in 1983 and 3 percent in 1983. “The enormous reduction of inflation included in the Reagan forecast is sharply at odds with virtually all predictions made by other economists recently,” Berry said.

Additionally, the preliminary Reagan forecast saw rising output along with falling inflation. According to Berry, real gross national product would rise 7 percent in 1982 and 4.5 percent in 1983. But most economists thought that a rapid fall in inflation would cause real output to tank. Arthur Okun of the Brookings Institution had calculated in 1978 that a one percent reduction in the basic inflation rate would cost 10 percent of GNP, which would sharply raise the unemployment rate.

The magnitude of the recession implied by the initial Reagan inflation forecast was too frightening to contemplate. This led to much negotiating among the troika members, with supply-siders arguing that scaling back the growth forecast could be politically crippling since that was the big payoff to a large tax rate reduction.

Something had to give with either the growth forecast or the inflation forecast, since they were viewed as being fundamentally at odds with each other. In the end, the growth forecast was lowered and the inflation rate was raised to be less in conflict. This split-the-difference approach satisfied neither the monetarists nor the supply-siders, but it did have one virtue – it reduced the budget deficit in Reagan’s budget projections. That is because real growth has little impact on the budget, but higher inflation was helpful because the tax code was not indexed for inflation in 1981. Hence, higher inflation would lead to bracket-creep as people were pushed into higher tax brackets, thus increasing Treasury’s revenues.

As one can see in the table, the supply-siders were more right than wrong. Inflation came down much more rapidly than expected. This caused the economy to crash, as the monetarists and Keynesians predicted, but the bounce back was very strong.

Economic Forecasts: Carter, Reagan and CBO, 1981 (percent)

| 1981 | 1982 | 1983 | 1984 | 1985 | 1986 | |

| Real GNP Growth | ||||||

| Carter | 1.7 | 3.5 | 3.7 | 3.7 | 3.7 | 3.7 |

| Reagan | 1.1 | 4.2 | 5.0 | 4.5 | 4.2 | 4.2 |

| CBO | 1.4 | 2.9 | 2.9 | 3.3 | 3.4 | 3.4 |

| Actual (GDP) | 2.6 | -1.9 | 4.6 | 7.3 | 4.2 | 3.5 |

| Inflation (CPI) | ||||||

| Carter | 12.5 | 10.3 | 8.7 | 7.7 | 7.0 | 6.3 |

| Reagan | 11.1 | 8.3 | 6.2 | 5.5 | 4.7 | 4.2 |

| CBO | 11.3 | 9.5 | 9.0 | 8.3 | 7.7 | 7.2 |

| Actual | 8.9 | 3.8 | 3.8 | 3.9 | 3.8 | 1.1 |

| Unemployment Rate | ||||||

| Carter | 7.8 | 7.5 | 7.1 | 6.7 | 6.3 | 6.0 |

| Reagan | 7.8 | 7.2 | 6.6 | 6.4 | 6.0 | 5.6 |

| CBO | 7.7 | 7.6 | 7.5 | 7.4 | 7.2 | 7.0 |

| Actual | 7.6 | 9.7 | 9.6 | 7.5 | 7.2 | 7.0 |

Sources: Carter forecast from its last budget released on January 15, 1981; Reagan forecast from its economic message released on February 18, 1981; CBO forecast from its economic outlook released on March 31, 1981.

According to Carter’s last budget, each one percentage point higher than expected inflation raised federal revenues by $11 billion – quite a lot when total revenues were around $600 billion. But this number is symmetrical, leading to lower revenues if inflation came in below forecast. This suggests that lower inflation added about $50 billion to the deficit in 1982 alone, about 40 percent.

A key reason for the rapid bounce back was from sharply rising defense expenditures, which rose from $134 billion in 1982 to $273 billion in 1986. According to Keynesian theory, increased government purchases of goods and services is the most effective countercyclical policy. So, unwittingly, Reagan’s policies provided a strong Keynesian kick to the economy just when it was needed.

The two of us were at loggerheads on these issues back in 1981, but with the passage of time it’s clear that we were both right to a certain extent. Inflation came down much faster than anyone thought at a much lower economic cost than imaginable. The tax cut deserves credit for this, as does the Keynesian medicine delivered by higher defense spending. The establishment was mostly wrong.

The lesson for today is that we shouldn’t be imprisoned by the conventional wisdom of establishment economists. When the magnitude of our economic problems is great, as it was with inflation in the early 1980s and stagnant growth now, bold policies must be enacted.

In 1981, Galbraith was executive director of the Joint Economic Committee and head of its Democratic staff. Bartlett was deputy director of the Joint Economic Committee and head of its Republican staff.