That trillion dollars’ worth of student loan debt “could very well be the next debt bomb for the US economy,” William Brewer, president of the National Association of Consumer Bankruptcy Attorneys, warned the Associated Press.

“‘As bankruptcy lawyers, we’re the first to see the cracks in the foundation,’ Brewer said. ‘We were warning of mortgage problems in 2006 and 2007. The industry was saying we’ve got it under control. Nobody had it under control. Now we’re seeing the same signs of distress. We’re seeing huge defaults on student loans and people driven into financial difficulties because of them.’”

Nigel Gault, chief economist at HIS Global Insight, wasn’t as pessimistic, but said the debt could “slam taxpayers and the still-ailing housing market.”

“‘When student loans don’t get repaid, debts are going to be transferred from the borrower to the taxpayer,’ further raising federal deficits, he said. And overburdened student-loan borrowers may fail to qualify for mortgages and ‘stay much longer in their parents’ homes,’ Gault said. Young adults forming households have historically been the bulk of first-time home buyers — and their scarcity could dampen any housing recovery.”

Although US Bank recently announced it was pulling out of the student loans market, and JP Morgan Chase said that as of July it will offer student loans only to existing customers, there remain plenty of big companies in the student loan game — but interest is usually much higher than the government rate (currently at 3.4 percent but set to double this summer unless Congress says otherwise).

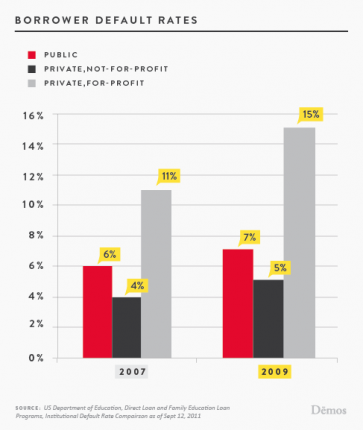

Click to enlarge

There are, however, two possible private banking alternatives that may ease high interest and the skyrocketing rate of default. According to the financial industry daily American Banker, “A number of smaller banks are considering making more student loans, even as bigger banks head for the exits…”

“’We’re still looking to see if it is something we want to stay in, but so far we’ve gotten good feedback,’ says Todd DeFee, the retail and student loan officer at Peoples State Bank in Many, Louisiana, which began making student loans for the 2011-12 academic year.”

Dan Kadlec at TIME magazine’s “Moneyland” blog reported an even more creative solution:

“… an innovative program called SoFi — short for social finance — is enlisting university alumni as benevolent lenders in a program that aims to keep student loan rates down. Alums contribute to a fund at their alma mater, which taps the fund to extend loans it wouldn’t otherwise offer — at rates below what is available in the commercial market. Participating alumni also serve as online mentors to students doing the borrowing, and the alums get paid back — plus interest.”

The program began at Stanford and next school year will be offered by some 40 universities, including Duke, Indiana, Wisconsin and UCLA. Interest runs “3 to 4 percentage points lower than many private loans.”

Alumni can invest IRA or 401 (k) assets with a projected annual return of 3.5 to 8 percent and help loan recipients with their job search after graduation. So you know you’re making a difference in the lives of students at your alma mater, which to our way of thinking, at least, is better — and cheaper — than having your name on a gym or stadium. Learn more about the program at SoFi.com.